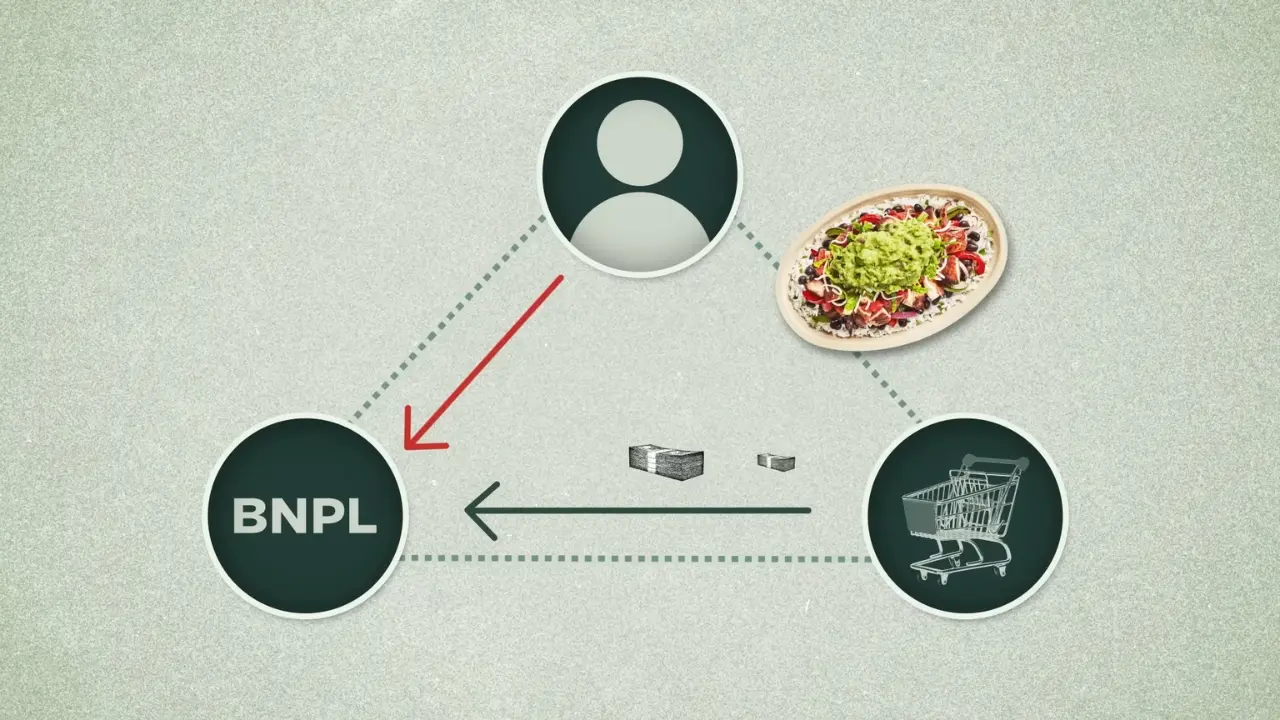

Buy now, pay later, often called BNPL, lets shoppers split purchases into smaller payments over several weeks or months.

Many plans advertise interest-free repayment when payments are made on time, but BNPL is still credit.

Shoppers are borrowing money for a purchase and agreeing to repay it later.

In the UK, at least 11 million people use BNPL. Growing use has raised concerns about missed payments, extra charges, and potential damage to credit scores.

Smaller payments can make a purchase feel easier to manage, but shoppers still need to check the full cost, repayment dates, and consequences before agreeing to a plan.

2026 Regulation Changes

Buy Now Pay Later (BNPL) borrowers will benefit from stronger protections from July 2026, when we start regulating the sector.

It will allow the 11 million people who use BNPL to make informed borrowing decisions to better navigate their financial lives.https://t.co/meQwpVZwm1

— Financial Conduct Authority (@TheFCA) February 11, 2026

Starting on July 15, 2026, UK BNPL regulation begins. Providers will need FCA authorization or must use a transition regime.

Lenders will also need to carry out affordability and creditworthiness checks before offering BNPL.

Affordability checks are meant to reduce unsuitable borrowing. Creditworthiness checks are meant to help lenders assess repayment risk before offering a plan.

For shoppers, that means BNPL may feel more like other types of credit at checkout.

Stronger shopper protections

New rules are expected to give shoppers clearer repayment information and better support if they fall into financial difficulty.

Consumers will also be able to escalate eligible disputes to the Financial Ombudsman Service.

Regulation should make BNPL clearer and safer, but it will not remove every risk. Shoppers will still need to decide if a purchase fits their budget before agreeing to split payments. BNPL attracts shoppers because it turns one purchase price into smaller scheduled payments. A shopper may want the item now but may not want to pay the full amount in one transaction. Spreading the cost across several weeks can feel easier, especially when the purchase is planned and the payments fit within a normal budget. For many shoppers, BNPL can also reduce the immediate pressure at checkout. Paying only part of the price upfront may make a larger purchase feel less stressful. Still, each installment is part of the same debt, so the full price has to be affordable before the shopper agrees to the plan. Several BNPL options appear often at online checkouts, and each one changes when the shopper has to pay: Each model can look simple, but shoppers still need to know the exact dates, payment amounts, and account used for repayment. BNPL is not limited to major household purchases. Many shoppers use it across everyday and occasional spending categories. BNPL can appear at checkout for clothes, jewelry, white goods, concert tickets, hotels, and takeaway meals. That wide availability can make BNPL easy to use without much planning. A shopper may start with one planned purchase, then add another plan for a smaller item. Over time, several low payments can become a larger financial commitment than expected. Retailers may offer BNPL because it can help increase completed purchases and average order values. A shopper who hesitates over a full price may be more likely to finish the order when the cost is split into smaller payments. For shoppers, that structure matters because any repayment issue is handled with the BNPL provider. Returning an item, raising a dispute, or missing a payment may involve both the retailer and the provider. Missed payments can make a simple checkout plan more expensive. Late fees may apply, and some missed or unpaid BNPL payments may also create marks on a credit file. That can make future borrowing harder or more costly. Fee rules can vary by provider, so shoppers should check the terms before accepting any plan: Small charges can add up quickly, especially when more than one BNPL plan is active. Automatic payments can create problems when a shopper has too little money in the linked bank account. A BNPL payment attempt may trigger an overdraft charge or a non-sufficient-funds fee. In that case, the shopper may incur costs associated with both the BNPL plan and the bank account. A missed automatic payment can also cause stress because the shopper may need to fix the BNPL payment, check bank charges, and still manage upcoming installments. Multiple BNPL plans can be difficult to manage because payment dates may overlap. A shopper may remember one installment but forget another due to the same week. Small payments can also feel harmless on their own, even when the combined total is high. Tracking becomes more difficult when purchases are made across different retailers and providers. One order may use Pay in 3, another may use Pay in 4, and another may be due within 30 days. Without a clear record, missed payments become more likely. Shoppers should focus on the total purchase price, not only the first installment. A small first payment can make an item feel cheaper than it really is. Before using BNPL, the shopper should check how much will be paid in total and how each payment fits into the coming weeks. Price checks matter most when the purchase is not essential. BNPL should not make an unnecessary item feel affordable just because the first payment is low. Repayment terms should be clear before checkout is completed. Shoppers should know each due date, each payment amount, and the account that will be charged. A shopper should also check if a payment date falls before payday or during a period with higher bills. Each installment should be affordable without using another loan, a credit card, or an overdraft. If repayment depends on borrowing again, BNPL may only move the debt instead of solving the cost problem. Budgeting should include all active BNPL plans, not only the newest purchase. A shopper may be able to afford one installment but struggle when several payments fall close together. A planned purchase gives the shopper more time to compare prices, check repayment dates, and confirm the total cost. Impulse use is riskier. Checkout can make BNPL feel quick and easy, but the payments still need to come out of future income. A simple tracking habit can reduce missed payments. Shoppers can use a note, spreadsheet, banking app, BNPL app, or calendar to record each amount owed and each due date. Keeping those details in one place makes it easier to see the total owed across all plans. Automatic payments can help shoppers avoid missed deadlines, but only when enough money is available in the account. Checking the balance before each due date can reduce the risk of late fees, overdraft charges, and non-sufficient-funds fees. Calendar alerts or app reminders can help, especially when several payments are due in the same week. Reminders should be set early enough to move money if needed. Several BNPL plans at once can create a larger monthly commitment than expected. A shopper should avoid opening new plans while older ones are still active unless the total cost is clearly manageable. Repaying BNPL with a credit card or another loan should also be avoided. That approach only moves the debt to another account and may add more cost. BNPL can be useful when it helps manage short-term cash flow for a planned purchase. Smaller installments can make budgeting easier, but only when every payment fits safely within the shopper’s income and expenses. UK rules beginning on July 15, 2026, should make BNPL clearer and safer. Even so, regulation will not remove the risk of overspending. Shoppers should treat BNPL like credit, not free money.

Why Shoppers Use BNPL

Common BNPL Payment Models

BNPL option

How it works

Pay in 3

Splits the cost into three payments, usually spread across a short period.

Pay in 4

Splits the cost into four payments, often with the first payment due at checkout.

Pay within 30 days

Delays the full payment until a later date instead of splitting the cost into several equal parts.

Purchases Covered by BNPL

Merchant and provider incentives

Key Risks

Klarna

Clearpay

May charge a £5 late fee after a seven-day grace period.

May charge £6 for a late payment.

Caps late fees at 25% of the order value.

May charge another £6 if the payment is still unpaid seven days later.

Allows a maximum of two late fees per order.

Uses caps that depend on order size.

Bank charges can add extra cost

Too many plans can become hard to track

What to Check Before Using BNPL

Repayment details

Affordability across every installment

Safer Ways to Use BNPL

BNPL is safer when it is used for planned purchases that can be repaid on time.Track every active plan

Prepare for automatic payments

Avoid stacking debt

Summary

{kind=link}