Shuffling between your student loans, auto loans, housing loans, and credit cards can be difficult. You might lose track of the payments and balances on outstanding debts. So, consolidating all these debts into a single loan seems to be an ideal choice as it helps you streamline your finances. However, it is not a one-size-fits-all solution.

Additionally, to decide whether debt consolidation is correct for you, you must consider factors like your financial goals and present financial state. Visit this page to know more about debt consolidation and seek expert help in Red Deer.

What is debt consolidation?

Paying off your debts using a new loan or a balance transfer credit card at a lower APR are popular ways of debt consolidation. You can either opt for a debt consolidation loan or get standard personal loans to pay off the debt. When you opt for a balance transfer credit card, you can get a 0% introductory APR (6 to 18 months).

Advantages of debt consolidation

There are several advantages of debt consolidation. Some of the most important ones are:

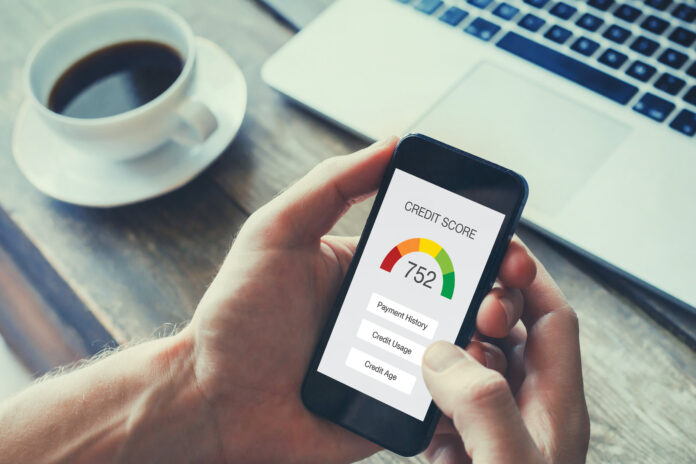

1. Improves your credit score

When you apply for a new loan, your credit score will temporarily fall due to hard credit inquiries. But when you opt for debt consolidation, it will improve your credit score in the long run in numerous ways.

For example, your credit utilization should always be under 30%. With the help of debt consolidation, this rate can be reduced significantly. Furthermore, paying on-time monthly installments to pay off the loan will also improve your credit score in the long run.

2. It helps to streamline your finances

As you combine multiple outstanding debts in a single loan, the interest rates will be less, and you only need to worry about one installment per month. It will also improve your credit score as the chances of forgetting or missing out on installments are also reduced.

3. You can expedite the payoff

If you notice that your debt consolidation loan has a lower interest rate than personal or individual loans, try making extra payments with the money you save per month. So with debt consolidation, you can pay off the remaining amount earlier, and therefore, in the long run, you can save much more on the interest.

But you need to remember that debt consolidation will lead to extended loan tenure. Thus, to get the maximum benefits, you have to try repaying your debt early.

4. Lower your interest rate

If you notice an improvement in your credit score, you can try to decrease your overall interest rate by consolidating debt. Therefore you will be saving a lot of money over the time duration of the loan, especially if you do not have a long-term loan.

However, you need to remember that some types of debt also come with higher interest rates. For example, credit card loans have higher interest rates than education loans or student loans. Combining multiple debts in a single loan will lower the overall interest rate.

5. Reduce monthly installments

Whenever you are consolidating debt, the overall monthly payment amount will decrease. This is simply because the future installments are spread out, and you also get an extended loan term.

Debt consolidation is beneficial from the viewpoint of monthly installments. However, you may need to pay a little more over the entire loan duration, even with a low-interest rate.

Cons of debt consolidation

Debt consolidation or balance transfer credit cards might seem like an easy way to pay off your debt. But there are certain risks and disadvantages.

1. Potentially increase your interest rate

This strategy is an intelligent decision if you are eligible for a low-interest rate. But if your credit score is not high enough, you may not qualify for the most competitive rates. Therefore you might get stuck with a higher interest rate than your current debts.

2. It comes with added costs

A debt consolidation loan also comes with processing charges, balance transfer fees, origination costs, and closing costs. So before applying for a debt consolidation loan with any lender or financial institution, ensure that you know about all the charges.

3. Encourage more spending

Once you start paying off credit cards and other debts using debt consultation, it might create an illusion that you have a lot of money. Therefore most borrowers might fall into debt traps. So you must make a budget to reduce spending so that you do not end up gathering more debt than you started with.

When is debt consolidation a good choice?

- Your monthly installments or payments (including all your EMI or mortgage) do not exceed 50% of your overall monthly income.

- Your cash flow is consistent and can cover all the payments towards your debt.

- Your credit score is pretty good, and you can qualify for a 0% credit or low-interest debt consolidation loan.

- You can pay off the consolidation loan within a maximum of 5 years.

However, it is advised to evaluate your spending habits and develop an efficient financial plan before consolidating your debt. While you cannot avoid some debts like medical loans, you can cut off amusement expenses which might result in overspending or otherwise financially dangerous behaviour.

When will debt consolidation not work for you?

Here is when debt consolidation would not work out for you:

1. You do not have an enormous amount of debt

If you have enough funds to pay off your entire credit card balance in the next 6 to 12 months, debt consolidation is not worth the effort and paperwork.

2. You have an average or poor credit score

Some money lenders or financial institutions might approve your debt consolidation loan even if you have a bad credit score. However, you will end up paying more interest which can potentially increase your monthly expenses and make the payments unaffordable.

3. You cannot manage your spending habits

A consolidation loan will free up available credit on your credit card, and you might start spending again. If you transfer your debt and then pile up more debts, you can be trapped in an endless debt trap. So it is always advised to address your current spending issues before applying for the loan.

Endnote

Paying accumulated debt will have a positive impact on your financial health. You will also learn to avoid racking up debts again in the future. So you must create a budget to stay on top of your expenses and avoid spending more via your credit cards than you can actually afford.

{kind=link}